How to Create a Debt Payoff Strategy That Works

A real debt payoff strategy that fits your actual life. 8 clear steps, 3 methods explained simply, and a stop-the-cycle plan. No perfect months required.

DEBTDEBT PAYOFF

Debt Series · Part 3 of 3 · ← Read Part 1 and Part 2 first

Let me tell you something I do not talk about enough.

I have done the shoveling problem. Not in theory. Actually done it more times than I can count tbh.

There was a season where I had debt and I was determined to get out of it. So I did what everyone says to do. I threw everything I had at it.

Every spare dollar.

Every bonus.

Every bit of breathing room went straight at the balance.

For a while it was working. I could see it coming down. I felt the momentum.

Then something happened.

I cannot even remember exactly what it was now, but something always happens. When it did I had nothing.

I had to go back to the credit card. And I stood there looking at that balance creeping back up genuinely feeling like I was in shambles. Like what was even the point.

Then COVID happened.

I know that sounds like a strange saving grace but hear me out. We were not going outside.

I was not spending on anything beyond bills and essentials. For the first time I was actually able to sustain the paydown because life was not showing up the way it normally does.

That was my turning point...

Not because I found a better strategy, because the circumstances changed in a way that gave the strategy room to breathe.

That moment taught me something important. The problem was never my discipline. The problem was a plan that had no room for real life .

In This Post

01 The real weight of carrying debt

02 Before the strategy: you have to stop digging first

03 What debt is actually costing you

04 See your full picture before you plan anything

05 The three methods explained simply

06 The WYT approach: rainy day fund first

07 Your step-by-step plan

08 Stop the cycle: staying debt free after the payoff

09 Patience in this journey

Before we talk strategy, I want to name what carrying debt actually feels like. Because I have seen it up close, in people I love and in my own life. It is not just a financial thing.

It shows up in your sleep, or the lack of it. You lie awake calculating, rearranging numbers in your head that never quite add up the way you need them to. It shows up in your body.

I have watched people I care about lose weight from the stress of it. Not intentionally.

The kind that comes from your nervous system being on alert for too long.

It shows up in your conversations, where you are technically present but your mind is three bills ahead of you.

There is a disassociation that sets in when the weight becomes too much.

You feel despair.

You feel like you made terrible choices, like you are behind everyone, like you somehow did this to yourself.

That feeling is real. You are not dramatic for feeling it.

The Real Weight of Carrying Debt

If you landed here without reading Part 1 of this series, it speaks directly to the feeling that this is your fault. It is not.

Part 1 addresses that and is worth reading alongside this one.

Debt is not just money.

It is a weight that goes everywhere with you until it is gone.

That is exactly why this strategy matters, not just for your account balance but for your sleep, your focus, and your ability to be present in your own life again.

Here is the piece that has to come before any method, any plan, any step-by-step.

You have to stop adding to the debt while you are trying to get out of it.

I have sat across from friends, family members, and colleagues over the years who were carrying serious debt, and one of the first things I always ask is whether they are still adding to it while they try to get out.

You cannot fill a bucket that has a hole in the bottom.

I saw a line recently that said it exactly right: "Avoid new debt while paying off debt. You first have to stop digging."

That means being honest about what is still creating new debt. The BNPL you keep reaching for when the month gets tight.

The credit card that becomes the emergency fund because there is no actual emergency fund yet.

The zero-interest promotion that feels free right now but has an end date buried in the small print.

On zero-interest promotions specifically, they can be a legitimate tool when used wisely. But if the period expires with a balance still sitting there, the interest often hits all at once, sometimes retroactively.

The bank is counting on you to miss that detail.

If you have ever found yourself paying debt down and ending up right back at the start, Part 2 of this series explains exactly why that cycle happens.

Stop the bleeding first. Then build.

Before We Talk Strategy: You Have to Stop Digging First

I studied accounting. One of the concepts that has stayed with me is the cost of debt.

Holding debt carries a literal cost. It is not just a number on a statement you manage month to month.

It is a resource being drained from you constantly, usually without you fully feeling it, because it is buried in a minimum payment that is mostly covering interest and barely touching the actual balance.

I came across a story recently where someone had made $6,500 in minimum credit card payments over three years.

The balance barely moved. That is exactly how compound interest works against you when you only pay the minimum. And I want to name the other cost that nobody puts in the contract.

I saw a line that stopped me: "Debt does not scream. It whispers. It quietly steals your sleep, your freedom, and your future."

That is real. I have seen it. Knowing this is not about shame.

It is about understanding what you are dealing with before you decide how to deal with it.

What Debt Is Actually Costing You

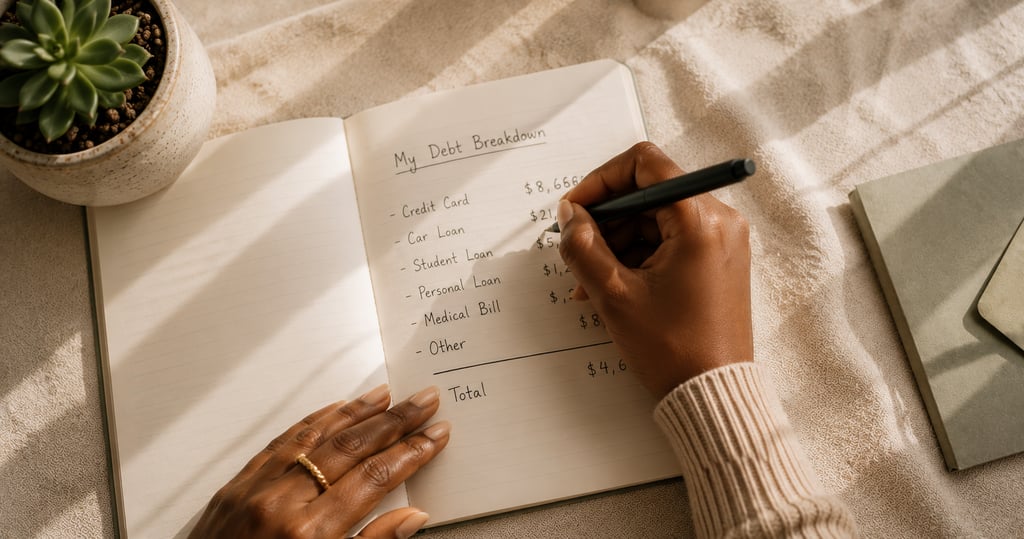

Before you pick a method or work through any steps, you need a clear and honest picture of where you stand.

Not a rough estimate or your best guess.

Every balance you carry on every account, all visible together so you know your real starting point.

The Financial Clarity Tool is how I looked at everything properly for the first time.

It shows every asset and every liability as balances in one private dashboard, with your net worth updating in real time.

As you work through your debt strategy and the balances come down, you update the numbers and watch your net worth shift in the right direction.

It does not calculate interest rates or minimum payments.

What it does is give you your full honest picture of what you own and what you owe, in one place, so you can build your strategy from clarity rather than anxiety.

Step Zero: See Everything You Owe in One Place

FINANCIAL CLARITY TOOL

Ready to see your full picture before you start your strategy?

Every asset and every liability together in one private dashboard. Your net worth updates in real time as the balances change. See where you actually stand before you build your plan.

The Three Methods Explained Simply

Snowball

Smallest balance

first

Pay minimums on everything, throw everything extra at the smallest debt.

When it clears, roll the payment to the next.

Built on momentum and early wins.

Avalanche

Highest interest

rate first.

Mathematically efficient.

You save more in total interest.

Slower to see the first win but the savings are real if you can stay with it.

Consolidation

Combine into

one.

One loan, one payment. Works when the rate is lower than your current debts.

Shop around. Read the terms for early repayment penalties.

Whether you choose snowball, avalanche, or consolidation, this stays the same.

Before you put a single extra dollar toward debt payoff, build a small buffer. Not a full emergency fund. A rainy day fund.

Just enough that when something arrives, and it will, you do not reach straight back for the credit card you have been trying to clear.

The difference between a rainy day fund and a full emergency fund matters here.

A rainy day fund is your first line of defence, a small pot of $300 to $500 that means one unexpected expense is an inconvenience rather than a crisis.

An emergency fund is the bigger goal, the three to six months that provides real stability.

This post covers the difference and how to build toward both.

Build the rainy day fund first. Pay your minimums while you do. Once it is there, start the strategy.

The WYT Approach: Rainy Day Fund Before Anything

The difference between a rainy day fund and a full emergency fund matters.

This post covers both and how to build toward them.

Work through this with your own numbers.

Step 1: List every debt you have.

Balance, interest rate, minimum payment for each one. All of it visible in one place.

Step 2: Know your minimum payment floor.

Add up every minimum. This goes out every month regardless of anything else.

Step 3: Build your rainy day fund first.

$300 to $500 separate and untouched before you start anything extra.

Step 4: Consider whether consolidation makes sense.

If a personal loan or consolidation product lowers your combined monthly payment or interest rate, it is worth investigating. Shop around and check terms for early repayment penalties.

Step 5: Choose your method.

Snowball, avalanche, or a hybrid. Choose the one that fits how you actually work.

Step 6: Calculate your real extra payment.

After minimums, after the rainy day fund is funded, after all your actual living costs, what is genuinely left? The honest number, not the optimistic one.

Step 7: Attack the target, minimums on everything else.

Every month. No negotiation with yourself.

Step 8: Roll the payment when a debt clears.

Take everything you were paying on it and move it straight to the next target.

Your Step-by-Step Debt Payoff Plan

Clearing the debt is one achievement. Staying out of it is the next one. I have watched people work hard to clear a debt and quietly rebuild it within a year.

Not because they were reckless. Because the habits that created the debt were still running in the background.

Stop the Cycle: Staying Debt Free After the Payoff

🚗 Stop financing depreciating assets

Phones, cars, furniture on BNPL. Build sinking funds for these instead so the money is already there.

🏦 Default to debit

Spending money you have rather than money you need to repay. That mental shift matters.

✂️ Remove easy credit access

Cut up the cleared cards. Remove from Apple Pay and Google Pay. Make credit spending a deliberate act.

🎯 Link your goals forward

Debt freedom clears the runway. The payment you have been making now goes toward building. Savings. A deposit. You already know how to redirect a monthly payment.

💳 Stop unnecessary BNPL

Buy now pay later is debt. It makes spending feel easier than it is. Only spend money you actually have.

👥 Build accountability

Forget willpower. You need a system and people working toward the same things. Find the community.

Sinking funds make the stop-the-cycle habits automatic. The sinking funds guide shows you how to set them up simply.

You did not get into this debt in a day. You are not going to clear it in a month. Sometimes it takes a year. Sometimes two or three.

Life keeps happening while you are paying it down.

The plan bends.

The timeline shifts.

That is not failure.

That is what building something real inside a real life looks like.

Patience in This Journey

"Me at 29: going through a divorce, $35,000 in credit card debt, starting over from scratch. Me at 34: married my soulmate, completely debt free, living the life I once prayed for. A lot can change in 5 years. Start."

A lot can change. The first move is starting. And you have everything you need to do exactly that.

THE Debt Series

Debt Payoff Methods - In Detail →

How to Choose The Right Debt Strategy

Coming soon

KEEP READING

DEBT SERIES

How to Choose the Right Debt Strategy

Coming Soon

WYT

Woman You Thrive is a personal finance brand built for women who earn but still feel stretched.

Created by someone still navigating the same tension, because the kind of guidance that actually helps comes from the inside, not from the other side.

IMPORTANT NOTE

This post is for educational purposes only and does not constitute financial advice.

Woman You Thrive is not regulated by the FCA or any financial authority.

For advice tailored to your specific circumstances please speak with a qualified financial professional.

SOURCES

StepChange, Women and Debt Report, 2025 · Young Women's Trust, Financial Worries Survey, 2025 · Fair4All Finance, Women in Financially Vulnerable Circumstances, 2025 · APA, Stress in America Report, 2025